.jpg)

Many high-income households face the same challenge each year: as income rises, so does the tax burden. Traditional planning tools—such as retirement contributions and charitable giving—can help, but they may not fully address the impact of higher marginal rates.

In certain situations, real estate ownership can offer additional tax planning opportunities. When structured carefully and supported by proper documentation, real estate investments may provide tax advantages while also contributing to long-term wealth accumulation.

This article is for informational purposes only and should not be construed as tax or legal advice. Tax outcomes depend on individual circumstances, and investors should consult their own qualified tax professionals.

This strategy is most relevant for households where:

Under IRC §469(c)(7), a taxpayer who qualifies as a Real Estate Professional may be able to treat certain rental real estate losses as non-passive. In some cases, this can allow those losses to offset other forms of active income. To qualify, the taxpayer generally must:

Because this designation is fact-specific and closely scrutinized, detailed recordkeeping and professional guidance are essential.

One reason rental real estate can be tax-efficient is depreciation: the IRS allows owners to deduct a portion of a property’s value over time. In some cases, investors may also consider a cost segregation study, which can accelerate depreciation by separating certain components of the property into shorter-lived categories (5, 7, or 15 years). Under current law enacted in the One Big Beautiful Bill Act, qualifying property acquired and placed in service after January 19, 2025 may be eligible for 100% bonus (first-year) depreciation, allowing accelerated cost recovery in the year of acquisition.

Eligibility depends on technical requirements, timing rules, and the taxpayer’s specific circumstances. Tax laws are subject to change, and investors should consult qualified tax professionals before implementing any depreciation strategy.

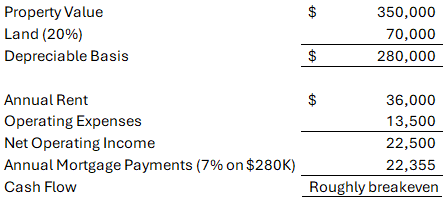

Hypothetical Illustration (For Example Only)

While depreciation reduces taxable income, the property quietly grows in value through two primary drivers:

If our example $350,000 property above appreciates at a rate of 3.5% annually, the value would increase to approximately $494,000 in 10 years, while the loan traditional loan balance would fall from $280,000 to approximately $235,000. That’s roughly $189,000 in equity growth, largely tax-deferred and supported by rental income.

When investors eventually sell real estate, tax treatment depends on many factors, but two common planning tools include:

Estate planning rules are complex and subject to change. Investors should work closely with qualified professionals.

For families exploring this approach, it is important to evaluate:

Real estate tax strategies can be powerful, but they are not one-size-fits-all and require careful implementation.

Real estate isn’t just a side investment for high-income families — it can be a central piece of a long-term wealth plan. By pairing one spouse’s earned income with the other’s active management, one can:

Done correctly, this strategy can turn ordinary tax dollars into appreciating assets — improving after-tax efficiency and supporting long-term wealth accumulation. If you’d like to learn more about how tax rules may interact with real estate investing, schedule an appointment with a GatePass Tax Services tax advisor.

GatePass Capital, LLC is a registered investment adviser; registration does not imply a certain level of skill or training. We also provide paid tax return preparation services through GatePass Tax Services, LLC and will not use or disclose your tax return information for non‑tax purposes without your written consent, as required by law (IRC §7216/§6713).

Unless otherwise indicated, commentary on this site reflects the personal opinions, viewpoints and analyses of the author and should not be regarded as a description of services provided by GatePass Capital or its affiliates. The opinions expressed here are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual on any security or advisory service. It is only intended to provide education about the financial industry. The views reflected in the commentary are subject to change at any time without notice. While all information presented, including from independent sources, is believed to be accurate, we make no representation or warranty as to accuracy or completeness. We reserve the right to change any part of these materials without notice and assume no obligation to provide updates. Nothing on this site constitutes investment advice, performance data or a recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Investing involves the risk of loss of some or all of an investment. Past performance is no guarantee of future results.

The best time to start is now. Personalized financial solutions don’t have to be difficult. We’d love to chat with you to learn more about who you are, what your goals are, and how we can help.

TALK TO AN ADVISOR