You completed your taxes expecting a refund, only to discover you instead owe thousands.

If this describes you, you’re not alone. Taxpayers who earn most of their taxable income as an employee typically assume their tax bill will be covered by the amount withheld throughout the year. However, some taxpayers still find themselves writing checks in April. There are a few common, easy to fix issues that can cause this. Addressing these could prevent surprise tax bills in future years.

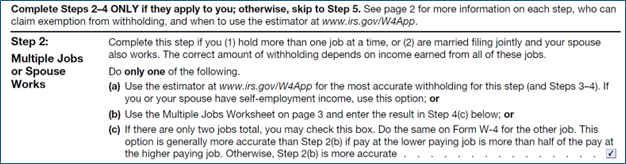

The most common mistake we see with payroll withholding is an incorrect Form W-4. This is especially common in dual income households. Married taxpayers who both work should ensure that they check the box in Step 2(c) (see below) or fill out the multiple jobs worksheet for their income taxes to be correctly withheld.

If both spouses work and they fail to check this box, then you will likely not have enough taxes withheld throughout the year and will need to pay the balance when you file your income tax returns. For example, if you and your spouse file a joint tax return and both make $100,000, approximately half of your income will be taxed at 12%, and the other half at 22%, for an effective tax rate of around 17%. If you fail to check this box, income taxes will be withheld at 12%, which matches the tax rate a married taxpayer whose spouse does not work would pay if making a salary of $100,000. This can result in a tax bill come April 15th.

For executives and other high earners, a large portion of their annual compensation is typically paid as a bonus. This can create a withholding issue because most payroll departments default to the IRS standard withholding rate for supplemental wages of 22%, regardless of what the taxpayer indicated on their Form W-4 or what tax bracket they fall into. For high earners this often leads to under-withholding of income tax.

For example, a taxpayer earning a $300,000 salary with a $300,000 bonus will have their bonus taxed in the 32% and 35% tax bracket, but their bonus may be withheld at the default rate of 22%. This could lead to an under-withheld tax of between $30,000 and $50,000, depending on what other income and withholding the taxpayer has.

The timing makes this worse. Bonuses are typically paid in February or March, but the tax bill isn’t determined until the following April; over a year later. By the time the taxpayer realizes they need to make a tax payment, the funds have often been spent or invested.

Like bonuses, some high-earning taxpayers receive grants of restricted stock units (RSU). These stock grants are taxed as earned compensation when the units vest, and like bonuses, most payroll departments withhold at a standard 22% by selling a portion of the stock to cover the taxes. Just like with large bonuses, 22% is often not enough to cover the tax on the stock grant for high-earning taxpayers.

If the stock grant is received in February, the tax is not due until the following April. This gap can be even more significant with RSUs, as the taxpayer may be forced to sell stock that they otherwise would not have sold to cover the unexpected tax shortfall, leading to taxable capital gains if the stock has increased in value, or being forced to sell the stock at a loss if the value decreased. Needing to sell stock that has decreased in value to cover the tax has an additional downside since the taxpayer received ordinary income upon vesting but is receiving a capital loss for selling.

Proactive planning around RSU vesting, by either requesting a higher withholding percentage or making quarterly estimated payments can help avoid the surprise tax bill and being forced to sell stocks you would have preferred to hold.

We have covered the most common reasons we see highly compensated taxpayers get hit with a surprise tax bill. Our experienced tax team is available to help you navigate these complex issues. We work year-round on proactive tax planning, allowing you to make informed decisions with your finances and avoid surprises.

GatePass Capital, LLC is a registered investment adviser; registration does not imply a certain level of skill or training. We also provide paid tax return preparation services through GatePass Tax Services, LLC and will not use or disclose your tax return information for non‑tax purposes without your written consent, as required by law (IRC §7216/§6713).

Unless otherwise indicated, commentary on this site reflects the personal opinions, viewpoints and analyses of the author and should not be regarded as a description of services provided by GatePass Capital or its affiliates. The opinions expressed here are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual on any security or advisory service. It is only intended to provide education about the financial industry. The views reflected in the commentary are subject to change at any time without notice. While all information presented, including from independent sources, is believed to be accurate, we make no representation or warranty as to accuracy or completeness. We reserve the right to change any part of these materials without notice and assume no obligation to provide updates. Nothing on this site constitutes investment advice, performance data or a recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Investing involves the risk of loss of some or all of an investment. Past performance is no guarantee of future results.

The best time to start is now. Personalized financial solutions don’t have to be difficult. We’d love to chat with you to learn more about who you are, what your goals are, and how we can help.

TALK TO AN ADVISOR