For many successful families, wealth planning often begins with investment management, tax efficiency, and estate planning. But there is another layer that deserves equal attention: protecting what has already been built.

In an increasingly complex world, affluent families may face a wide range of risks, including litigation, business liability, creditor claims, divorce, fraud, concentrated real estate exposure, and family-governance challenges. Asset protection planning is designed to help reduce those vulnerabilities before they become urgent.

At GatePass Capital, we believe wealth planning should be coordinated, forward-looking, and grounded in each client’s best economic interests. Asset protection is not about hiding assets or reacting after a claim appears. It is about designing a thoughtful structure around your financial life so your wealth is better positioned to support your family, your goals, and your legacy over time.

Asset protection is the process of legally structuring ownership, liability, insurance, and estate planning strategies to help shield family wealth from unnecessary exposure. The objective is straightforward: separate vulnerable assets from potential claims where appropriate, while maintaining a structure that still supports control, flexibility, tax planning, and long-term family objectives.

For example, a family that owns rental real estate, a closely held business, taxable investment accounts, and personal property may face different types of risk across each asset category. A strong plan does not treat those assets the same way. It evaluates how each asset is owned, who controls it, what liability is attached to it, and whether the family’s current insurance and estate plan are sufficient.

Common tools may include:

Asset protection works best when it is built proactively. Once litigation, a creditor claim, or financial dispute has already surfaced, the available options can become significantly more limited.

Greater wealth often brings greater complexity. For high-net-worth families, risk may come from more than market volatility. It may come from business ownership, professional liability, family dynamics, concentrated holdings, real estate, or public visibility. Some of the most common risk areas include:

Affluent families may be more visible targets for personal injury claims, business disputes, professional liability, or property-related litigation.

Business owners, executives, physicians, real estate investors, and entrepreneurs may have risks tied to operating entities, professional decisions, employees, partners, vendors, or personal guarantees.

Divorce, blended families, second marriages, financially inexperienced heirs, or spendthrift beneficiaries can create planning challenges that extend beyond traditional investment management.

A family that holds significant wealth in one business, one real estate portfolio, or one low-basis stock position may need customized planning around liquidity, tax exposure, control, and creditor protection.

As wealth grows and family structures expand, scams, elder exploitation, and poor decision-making can become meaningful threats to long-term financial security. The goal is not to eliminate every risk. That is not realistic. The goal is to understand where the family is exposed and build layers of protection that make the overall plan more resilient.

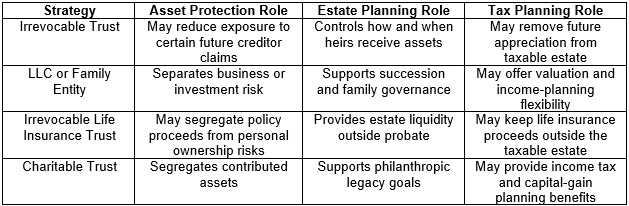

A strong asset protection plan is rarely built around one technique. It usually combines several strategies, each serving a different role.

Insurance is often the starting point because it provides liquidity when a covered claim occurs. Depending on a family’s situation, coverage may include:

Umbrella insurance can be especially valuable because it provides additional liability coverage above the limits of certain underlying policies. For many families, it is one of the most efficient first steps in a broader risk-management plan.

That said, insurance has limits. Policies contain exclusions, coverage caps, and claims procedures. Insurance should be viewed as one layer of protection, not the entire plan.

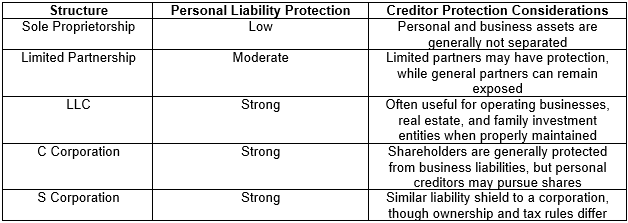

For business owners and real estate investors, entity structure can have a major impact on liability exposure. A sole proprietorship generally offers no legal separation between the owner and the business. By contrast, an LLC or corporation can create a liability shield when properly established, funded, and maintained.

Entity choice should be coordinated with tax planning, operations, governance, and succession objectives. The entity must also be respected in practice. Commingling funds, ignoring formalities, or personally guaranteeing obligations can weaken the intended protection.

Trusts can play an important role in protecting family wealth, especially when planning for future generations. Certain irrevocable trusts may help separate assets from an individual’s personal estate and reduce exposure to future creditor claims, depending on state law, timing, trust design, and how the trust is funded.

Trust planning may also help address beneficiary-specific risks, including:

An asset protection trust may be appropriate in certain circumstances, particularly for families with meaningful wealth, business ownership, professional liability, or concentrated risk. However, these strategies require careful legal guidance and must be implemented before a claim arises.

How assets are titled can materially affect risk, control, probate, and estate-planning outcomes. For example, joint ownership may simplify transfer at death, but it can also expose assets to a co-owner’s creditors. Some states provide special protections for a primary residence, retirement assets, life insurance, annuities, or property owned by married couples as tenants by the entirety. Asset titling should not be an afterthought. It should be reviewed alongside the estate plan, tax strategy, and risk-management plan.

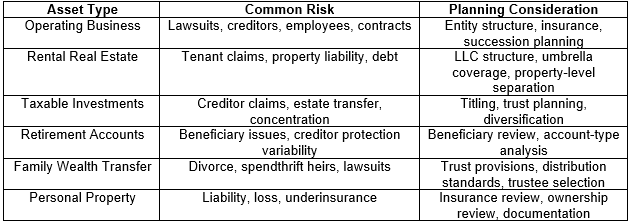

Different assets carry different risks. The protection strategy should reflect the asset.

Business owners should evaluate whether operating assets, intellectual property, real estate, and excess cash are held in the most appropriate structure. In some cases, separating operating risk from valuable assets can be an important planning step.

Key considerations include:

Real estate can create liability through tenants, visitors, employees, contractors, environmental issues, debt, and property-level claims. Families with multiple rental or investment properties may consider using separate LLCs or other structures to isolate risk by property or property group. This can help prevent a liability issue at one property from threatening the entire portfolio.

Market risk is not the only consideration for investment assets. Families should also consider creditor protection, tax treatment, beneficiary designations, account ownership, and estate transfer. Retirement accounts may receive certain creditor protections under federal or state law, though the level of protection can vary by account type and jurisdiction. Beneficiary designations should be reviewed regularly and coordinated with the estate plan.

Primary residences, vehicles, collectibles, boats, aircraft, and other personal assets may create liability or require specialized coverage. In some cases, ownership structure and insurance planning should be reviewed together.

Even well-intentioned plans can fall short if they are incomplete or poorly maintained.

Asset protection should be proactive. Transferring assets after a claim arises can create legal issues and may be challenged as a fraudulent transfer.

Insurance is important, but it may not cover every risk or claim amount. A more resilient plan combines coverage with ownership structure, legal planning, and ongoing review.

A trust only controls the assets that are actually transferred into it. If accounts, real estate, or ownership interests are never retitled, the intended protection may not exist.

Commingling funds can weaken the liability protection of an LLC or corporation. Business accounts, records, contracts, and formalities should be kept separate.

Protecting wealth during your lifetime is only part of the equation. A complete plan also considers how assets will be protected after they pass to children, grandchildren, or other beneficiaries.

Asset protection should not sit in isolation. The best planning often combines risk management, tax planning, estate strategy, and investment management into one coordinated framework.

The right mix depends on the family’s net worth, balance sheet, state of residence, business interests, risk exposure, estate objectives, and tax profile.

Asset protection is not about fear. It is about preparation.

Families work for decades to build wealth, support loved ones, grow businesses, and create opportunities for future generations. A thoughtful protection plan helps ensure that one lawsuit, creditor issue, family dispute, or planning mistake does not unnecessarily disrupt that progress.

At GatePass Capital, we help clients evaluate the full picture: investments, estate planning, tax strategy, risk management, business interests, retirement needs, and family priorities. Our role is to help coordinate advice around your best economic interests and bring structure to the decisions that matter.

For families with meaningful wealth or complex assets, asset protection should be reviewed before risk becomes reality.

If you own a business, hold investment real estate, have concentrated wealth, or want to strengthen your family’s long-term financial plan, now may be the right time to review your current structure.

A good starting point includes asking:

The strongest plans are built before they are needed. If you want help protecting what you've built, reach out to a GatePass wealth advisor today.

Unless otherwise indicated, commentary on this site reflects the personal opinions, viewpoints and analyses of the author and should not be regarded as a description of services provided by GatePass Capital or its affiliates. The opinions expressed here are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual on any security or advisory service. It is only intended to provide education about the financial industry. The views reflected in the commentary are subject to change at any time without notice. While all information presented, including from independent sources, is believed to be accurate, we make no representation or warranty as to accuracy or completeness. We reserve the right to change any part of these materials without notice and assume no obligation to provide updates. Nothing on this site constitutes investment advice, performance data or a recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Investing involves the risk of loss of some or all of an investment. Past performance is no guarantee of future results.

The best time to start is now. Personalized financial solutions don’t have to be difficult. We’d love to chat with you to learn more about who you are, what your goals are, and how we can help.

TALK TO AN ADVISOR